FactSet: From Quality-at-Any-Price to Moat-at-a-Reasonable-Price

Why an AI panic and a growth scare may have created a durable compounder on sale

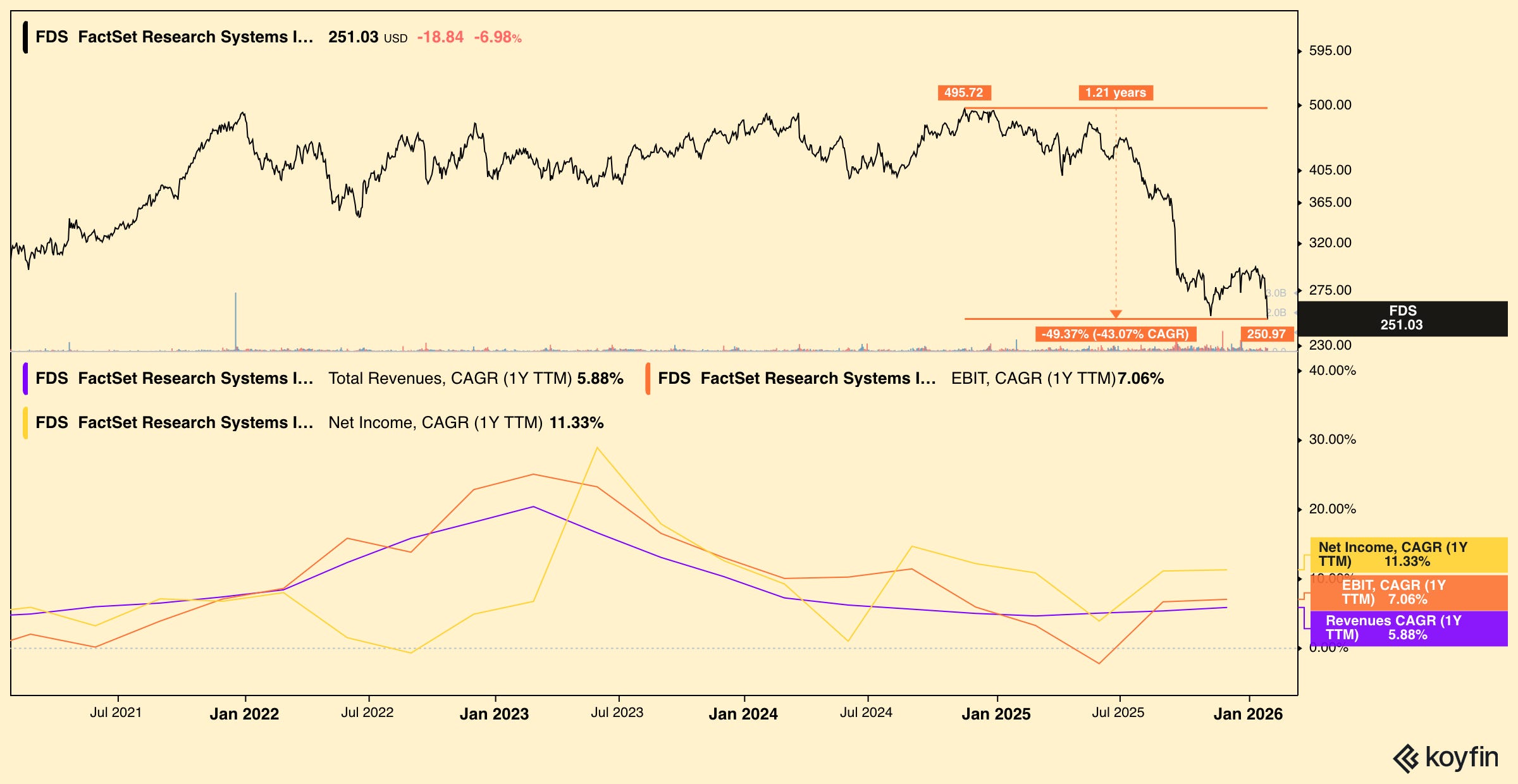

Overview

FactSet (FDS) is a high‑quality, wide‑moat financial data and analytics platform that has just gone through a brutal re‑rating. From a peak near $500, the stock has fallen 50%, compressing its multiple from a quality-at-any-price premium into not quite a GARP play, because growth is lacking, but more like a MARP (moat-…